I usually don't get into the middle of topics like these. Today, for some reason, this irked me in a way unlike other comments of its kind, probably because of the individual behind these statements:

Ben Carson is a renown neurosurgeon at Johns Hopkins, with an impressive range of publications and Chair appointments and whatnot. I'm not going to go into what a big deal he is, because you can probably see that on his wikipedia page. Or you can read one of his books and he'll tell you himself. The man has power in the medical community, and he has a reputation of being a technically gifted surgeon, good enough that people would seek him out when they had a particularly awful or rare disease. The man's 61 years old though, near retirement, and of late he has started to step from the medical world to the political realm as one of the republicans' alleged championed candidates for the next presidential election. He's a Seventh-Day Adventist Christian, and he's not afraid to let the world know his religiously-guided views.

Here's where I find his comments upsetting and ironic (besides comparing gay marriage with NAMBLA and bestiality, because, well, I assume most rational people think that's fucked up): In the clip, Carson describes the establishment of heterosexual marriage as a "well-established fundamental pillar of society" and says that gays, pedophiles, and zoophiles (had to look that one up) "don't get to change the definition [of marriage]." He goes on to say that he's against anyone who "wants to come along and change the fundamental definitions of the pillars of society."

Let's take a look at those statements. It seems to me that by "pillars of society" Dr. Carson is referring to the Seven Pillars of Society as defined by Christian followers. The Seven Pillars are: Government, Family, Business, Media, Education, Religion, and Arts & Entertainment. We could also take "pillars of society" to mean the American traditions that have been upheld for generations, which have become ingrained in our culture through the centuries. Either way, his argument here doesn't make much sense to me.

In his books, Dr. Carson relates the many barriers he had growing up. He was from a poor family, raised by a single mom, and he was an African American during a time that the vast majority of doctors were white. Color barriers were possibly the strongest walls he had to break through to become a physician, and he describes holding fast to his religion, which got him through many of his darkest hours. So what, you may ask?

Back in the day, slavery was defended with religion. Proponents would cite Bible verses to justify keeping slaves, to justify their mistreatment, and to sometimes justify raping them:

"slaves, obey your earthly masters with fear and trembling" (Ephesians 6:5), or "tell slaves to be submissive to their masters and to give satisfaction in every respect" (Titus 2:9).

If you asked slaveholders, opponents of slavery could be described as wanting to "change the fundamental pillars of society", to destroy the masters' livelihood and to directly disobey the Word of God. So what happened? Why don't we have slaves anymore? Those questions might anger some individuals, because the answer is so blatantly clear. A morally good society toppled the senseless, racist, absolutely evil practice of servitude with a Civil War, though the war for true integration of African Americans continued into the 20th Century (and still continues to this day, to be honest). Dr. Ben Carson was born (in 1951) at an interesting time, a time of intense racism, but a time where early integration was taking hold. He reaped some of the benefits of the bloodshed during the 19th Century, where those "pillars of society" were shaken and eventually brought to the ground. He could become a neurosurgeon because those pillars no longer existed and were ever-so-slowly being replaced by new ones.

Now Ben Carson is trying to reinforce other pillars, to prevent some individuals from achieving the same equality that he dreamed of as he went through school. To continue his analogy, and to make my views perfectly clear if they weren't before, I think that some ugly, moldy, fading, crumbling pillars of society need to be hit with a wrecking ball so newer, stronger ones can be built in their place to support the modern architecture of society. Interracial marriage and women's rights, as two examples, are other pillars recently constructed from the wreckage of age-old traditions. Not many sane people would argue that women need to stay in the kitchen and tend to children at home forever, but that wasn't the case only a few generations ago.

Unfortunately for Dr. Ben, not everyone seems to share his opinions on gay marriage. He was scheduled to speak at the commencement for Hopkins Medical School this year, but due to student protests over his comments, and the above statement by the dean of the school, he decided to step down from the job. Here's a quote from his apology letter to Johns Hopkins:

"Although I do believe marriage is between a man and a woman, there are much less offensive ways to make that point. I hope all will look at a lifetime of service over some poorly chosen words."

And here I will make my last point. The "poorly chosen words" that he describes refers to comparing homosexual individuals to pedophiles and zoophiles, not to his "pillars of society" comment. Not only is he an ass for saying these demeaning comments, to me it appears that his moral compass has somehow lost its center, if it was ever even magnetized correctly in the first place. For me, it is not these "poorly chosen words" that so angers me, it's his deep-rooted opinion of homosexuals within the recesses of his heart that truly upsets me. It upsets me that this man is (was?) a highly respected neurosurgeon, representative of not only himself or Johns Hopkins, but in a way a representative for physicians and the medical community, whether he wants to be or not. Even a lifetime of service, or a CV 60 pages long, doesn't change the fact that I no longer have a desire to shake his hand.

I wish to say, from a lowly soon-to-be doctor with respect for every patient regardless of their race, gender, or sexual orientation, to a seasoned, respected, accomplished, world-renown neurosurgeon with a giant CV:

A while back, Teej and I were discussing the Affordable Care Act (ACA) and what it could mean for him. I'm not sure my explanation of how it works at a practical level was particularly clear or useful. But this medium is a little more conducive to presenting complex concepts. So I'm going to try to lay it out here and illustrate in concrete terms what it means, using real live (not hypothetical) newly available numbers to go with it. This will all be from the perspective of an unmarried guy in his '20s, as that seems to be the readership, though the only thing that really changes for different household sizes is the particular numbers.

One disclaimer before we begin: this post is about the new insurance marketplaces being set up as we speak, and most people will not be buying through those marketplaces. If your income is lower than the thresholds we're going to talk about below, you'll be eligible for Medicaid--though the exchange website will still probably be your first stop on the way to getting coverage. The politics and policy of the Medicaid expansion are a topic for another post (or series of posts!). And if you get insurance through work, this won't apply to you. This is really about what happens to people who have to buy insurance on their own.

By way of introduction to all this, it's important to remember the basic change that's happening later this year and why. Most people with private health insurance have it through their jobs in the form of employer-sponsored insurance, the red piece of the pie to the right. While the ACA does affect those people a bit (mostly in the form of some new benefits and consumer protections), the insurance reform provisions of the law are primarily aimed elsewhere: at the individual market, the place where people who need to get insurance on their own shop for it.

In most states, people shopping in the individual market have far fewer consumer protections available to them than do people with employer-sponsored insurance. The insurance policies themselves are skimpier, premiums are more volatile, and "pre-existing condition" is a much deadlier phrase. And since those folks are buying insurance on their own (hence the name "individual market"), they lack the "strength in numbers" advantages that people in employer-sponsored group coverage enjoy. Only about 5% of the population currently gets health insurance through the individual market but expansions in private health insurance coverage will swell the ranks of the individual marketeers. But beyond people simply not being able to afford coverage or being turned away for pre-existing conditions, the individual market doesn't act much like a market:

One of the great challenges in buying health insurance has been a highly fragmented market. Individuals and group purchasers lack a reliable means for seeing their choices in one place and in a manner that allows them to compare what the plans cover, which providers are in various plans’ practice networks, how cost-sharing might differ, and how numerous competing plans might compare on key measures of quality performance. Nor has there been an active, consumer-oriented system for assuring that insurance plans that are offered in the individual and small group markets provide comparable coverage, cover the benefits that are considered essential to any health insurance plan, have accessible provider networks, and are accountable for specific measures of health care quality.

That's from an excellent and relatively succinct overview of what problems health insurance exchanges--recently re-branded by HHS as Health Insurance Marketplaces--are being created to correct and how they're going to do it. The short, short version is that they're creating competitive, transparent, consumer-friendly marketplaces where the playing field is level between you and the insurance companies.

Starting in October of this year, people will be able to start shopping for insurance through them. While they were originally envisioned as being primarily state-designed and state-operated, political intransigence has led to HHS having to step up and run federally-facilitated exchanges in 33 states. But that's a story for another time. Let's get into what's going to be sold in these marketplaces.

Tiers of a Clown

While factors like your gender and

medical history won't raise your premiums,

smoking will.

Since part of what makes a market a market is offering consumers intelligible and meaningful choices, exchanges will have a way of organizing health insurance plan options to allow more apples-to-apples comparisons between them. Plans will be grouped into four tiers, named after metals:

Platinum

Gold

Silver

Bronze

The tiers represent varying levels of generosity across the plans. Note that this does not mean a platinum plan is offering more benefits than a bronze plan. All plans are required to offer a set of essential health benefits, a fairly comprehensive set of services across ten categories of coverage. Plans can offer more but they can't offer less.

The metal level instead refers to the health plan's actuarial value, a measure of what proportion of the costs for those benefits it can expect to cover for a given population. A bronze plan, for instance, will have roughly a 60% actuarial value, meaning that it will pay 60% of the costs of those benefits and enrollees will pay for the remainder of the costs through deductibles and coinsurance when they go to get care. These plans are the skimpiest metal plan, not in the sense that they cover fewer benefits but in the sense that they require you to pay for a larger proportion of them if you need to use those benefits. The tradeoff is that the monthly premiums will be lower.

Silver plans have a 70% actuarial value, gold 80%, and platinum 90%. As you climb the metal ladder, the monthly premiums increase but so does the generosity of the plan; if you need to use covered medical services, swankier metal plans will pick up more of the tab. Silver plans, as we'll see, are sort of the default option but shoppers in the exchanges can choose a plan from any metal tier they like.

The Tax Credit

If you're eligible, when you shop for coverage through an exchange a subsidy will be made available to you to help you pay for an insurance plan (and if you're eligible for Medicaid instead, the exchange application process will let you know that and help you in enroll in it). Technically you'll get a refundable, advanceable tax credit. Refundable because its value can actually exceed your total tax burden, in which case the government is giving you money. Advanceable because you don't have to wait until tax time to get it back, it's available upfront when you go to buy insurance--so none of that money actually has to come out of your pocket.

Though HHS is still working the kinks out of their draft of the application process, they've produced a video to show you what the process will be like for a single person:

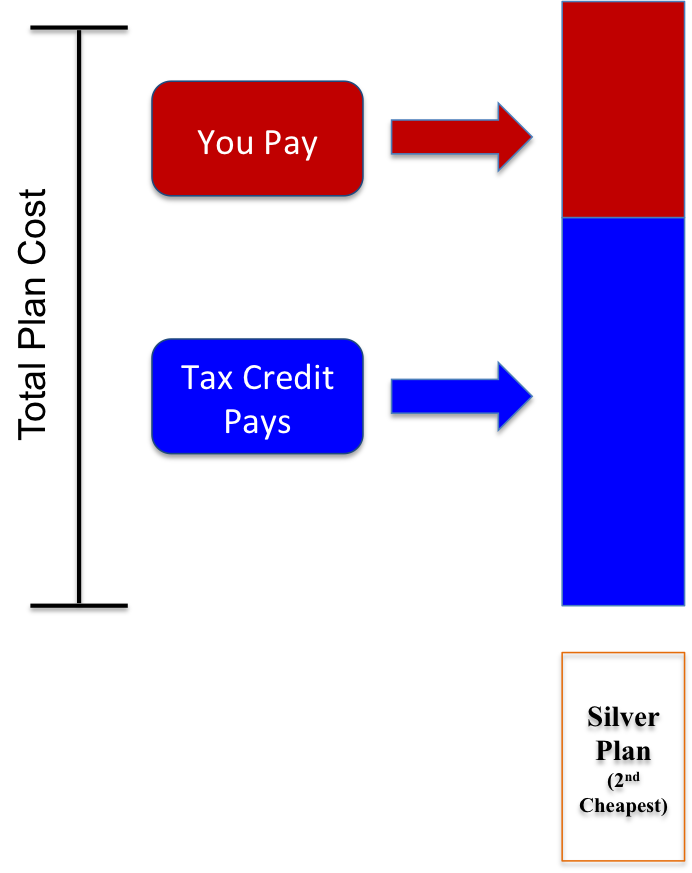

But how does the tax credit work? Its value will be pegged to the cost of a certain silver plan in your marketplace--the second cheapest silver plan--through a fairly simple formula:

[Value of the federal subsidy] = [Cost of 2nd cheapest silver plan] - [your required contribution]

What that says it that there's some amount of the premium you'll have to pay for the second cheapest silver plan, and then the federal government will pay for the rest of it. Or in picture form:

As we'll see a little more clearly later, this particular insurance plan just serves as the benchmark for calculating the size of the federal subsidy to which you're entitled. You don't have to actually buy that particular silver plan to get the tax credit.

Structuring the subsidy this way helps to retain the incentives and dynamics that should undergird markets. More expensive plans cost consumers more, as they should. Consumers still have incentives to buy less expensive plans (or at least carefully weigh the costs and benefits of buying more expensive plans) and insurers still have an incentive to offer the cheapest plans in the market, because those are the plans that will be most attractive to shoppers--even the subsidized ones.

Show Me the Money!

I mentioned that you have a required contribution to your premium which--along with the price of the second cheapest plan available to you--determines the size of the tax credit you get. If your income is under four times the poverty line, your contribution is limited to a certain percentage of your income. The particular percentage will depend on your income; it increases on a sliding scale, as you can see from this table pulled right from the ACA:

In the case of household income (expressed as a percent of poverty line) within the following income tier:

The initial premium percentage is--

The final premium percentage is--

Up to 133%

2.0%

2.0%

133% up to 150%

3.0%

4.0%

150% up to 200%

4.0%

6.3%

200% up to 250%

6.3%

8.05%

250% up to 300%

8.05%

9.5%

300% up to 400%

9.5%

9.5%

A major part of the "affordable care" bit of the law's title is a reference to this table. The idea is that people buying health insurance in an exchange will have their income protected, i.e. the amount they have to spend on health insurance premiums will be capped at a certain percentage of their income.

So for instance someone at 150% of the poverty line will not be asked to pay more than 4% of his income on health insurance premiums. Meanwhile someone at 250% of the poverty line won't be asked to pay more than 6.3% of his income on premiums.

Now since we're thinking specifically of a single person, we can translate those percentages into dollar amounts. I'm going to base this on the 2013 poverty thresholds, which have the poverty line at $11,490. It might be slightly higher next year when the tax credits and exchanges become available, but that won't change what we find here very much. Here's the table above, recast in terms of the caps on what folks of various incomes pay on their premiums:

In the case of household income within the following income tier:

Maximum monthly premium (low end)

Maximum monthly premium (high end)

Up to $15,282

$25

$25

$15,282 up to $17,235

$38

$57

$17,235 up to $22,980

$57

$121

$22,980 up to $28,725

$121

$193

$28,725 up to $34,470

$193

$273

$34,470 up to $45,960

$273

$364

Remember that those numbers rise smoothly on a sliding scale within each tier. This should give you a rough estimate, based on your income, of the premium you would be asked to pay for the second cheapest silver plan in your area.

Not So Fast!

Seems simple enough, right? You don't even need to know what the actual premium the insurer is charging is going to be because your personal contribution to your premium is spelled out right there in black and white. But it can be as simple or complicated as you like.

This is because of the way the value of your tax credit is calculated. As we saw, the federal government is offering you some fixed sum of money equal to [Cost of 2nd cheapest silver plan] - [your required contribution]. That means if you buy that second cheapest silver plan, all you pay for your premium is your required contribution, as pulled from those tables above.

But you don't have to buy that particular plan. You're well within your rights to buy a more expensive silver plan, or a gold or platinum plan. The government still gives you that fixed amount of money and you have to cover the rest of the cost of the plan. Obviously that means you would end up paying more--maybe a lot more--than the tables above would suggest.

On the other hand, you could also opt for a cheaper plan. That might be the very cheapest silver plan or a bronze-level plan. In that case, you still get the full value of the subsidy, meaning your own required contribution is going to go down.

Let's All Go to Vermont

Let's illustrate with a real example using actual premium values. Right now exchanges are soliciting interest from insurance companies who might participate later this year and they're asking them to submit information on how much they will charge in premiums. Most states (and the federal government) are going to let those numbers trickle in over the next 1-3 months. But one state, Vermont, has finished that process and recently made the numbers public.

They put together two tables collecting those premium numbers here. (As an aside, you'll notice that there are two tables because one lists prices for Standard Qualified Health Plans (QHPs) and one lists prices for Non-Standard Qualified Health Plans. In putting out feelers to insurance companies to see if they would sell in the exchange, Vermont made clear that participating insurers will have to sell plans with certain standard designs, meaning the plans' deductibles and co-insurance requirements for different services have to be what the state specified. You can see the specifications for the standard plans starting on page 50 of this document. However, in addition to those plans the insurers are allowed to innovate and sell other "non-standard" plans with different designs. Both kinds of plans "count" when figuring out what the cheapest silver plan is.)

Let's look at just silver plans available to a single person shopping in the Vermont exchange. Between the two insurers selling them, Blue Cross Blue Shield of Vermont (BCBSVT) and MVP, there are eight different silver plans you could choose from. The second cheapest one on the market is BCBSVT's non-standard "Blue for You" plan (listed on the second page of that document), weighing in at $413.03 per month.

So now we have the value of the tax credit you have to play with, dear Vermonter. It's going to be $413.03 minus your required monthly contribution. So let's suppose you're making exactly $22,980. Convenient! According to our table, that means that if you buy that Blue for You plan your contribution to the premium will be $121 per month. The government's subsidy to you is $413 - $121 = $292. (For simplicity's sake, let's ignore the 3 cents).

But maybe you don't want to buy the Blue for You silver plan. You're an extravagant type and you want the top of the line: MVP's $614.77 per month platinum plan. You can go buy it and put the government's $292 toward it but that means you're on the hook for paying the other $322.77 every month.

Or maybe you want to go the other way. You're looking to minimize your own premium contribution and so you hone in on the cheapest metal plan on the market: BCBSVT's "Blue for You CDHP" bronze plan. That's $350.08 per month. You still get to put the government's $292 toward that plan, which leaves you on the hook for only about $58 per month. Significantly less than the $121 you'd be paying if you went for the silver plan to which the subsidy's value is pegged. Indeed, for people with lower income than you (who are thus eligible for a larger federal subsidy), they can get their own contribution down to zero for some of the bronze plans. Of course, their own required contribution for the benchmark silver plan is correspondingly smaller than yours and so they don't lose much in paying it and opting for the more generous coverage of a silver plan.

Back to the figure, this time expanded. You can see from the varying total heights of the bars below the difference in total plan costs from plan to plan. The platinum plan on the far right is the most expensive and so it's correspondingly the tallest. It also requires you to pay the most for your premiums, since the federal share of the costs (the tax credit) has a fixed value.

Because the value of the tax credit is pegged to the value of the second cheapest silver plan, its value is the same regardless of which plan you buy.

As this visually (hopefully) makes clear, you can vary your actual monthly contribution to the premium, represented as the red share of the total premium, by choosing cheaper or more expensive insurance plans.

The numbers in this section, of course, are unique to Vermont. The actual premiums and the number of plans to choose from will vary from state to state, although the numbers aren't likely to vary substantially from the Vermont examples we've looked at here.

A word of caution

It's worth noting that there's a special benefit to buying a silver plan. The ACA doesn't just provide subsidies for health insurance premiums, it also provides subsidies for cost-sharing. That means it will help you pay for part of your deductible if you need care, as well as part of your co-pays or co-insurance. However, while the premium tax credit can accompany you to any coverage tier and be applied to any plan, the same isnottrue of the cost-sharing subsidies: the cost-sharing subsidies are only available if you buy a silver plan. If you buy a bronze plan to get your premium contribution as low as possible, should something happen and you actually need care you'll have a very large deductible (in Vermont's standard bronze plan designs, the deductible is around $2,000) to grapple with and no help in doing so. Something to keep in mind.

Secret Option F

There's one other option in the exchanges I haven't mentioned. This is a plan type that's available only to people under 30 (or people who otherwise don't have access to an affordable plan). It's called a catastrophic plan and is designed specifically to offer less generous coverage than any of the metal tiers. Why is this desirable? It was felt that since young people are less likely to use coverage, they'd be more willing and eager to buy a lower-premium, high-risk "young invincibles" plan than more standard coverage.

However, if you choose the catastrophic option you get no financial assistance. While you can take your federal tax credit and put it toward any plan bronze through platinum, you cannot put it toward a catastrophic plan. The entire premium is on you. And it probably goes without saying that you'll also have no help in paying for the cost-sharing, which by design is sizable in these plans.

Everybody Got That?

Hopefully this was clear enough to give you a sense of what you can expect if you end up buying insurance through an exchange. Comments welcome--if something's unclear or underdeveloped, I'm happy to revise.

One more thing: if the exchange does its job right, you won't actually have to know any of this. You'll fill out the application and it will figure out what you're eligible for and explain to you what you can and cannot apply it to. You won't need to sit there with a calculator and a set of tables to figure things out.